: Why the drop in the unemployment rate to 6% doesn’t mean very much

The Issue

The state of the labor market reflects the state of the economy and, even more important, the human cost of recessions or the benefits of booms. Accordingly, the unemployment rate is one of the most closely watched economic statistics.

But it is becoming more widely recognized that the most frequently cited official unemployment rate misses a lot of people. Problems with measuring labor-market slack have been particularly acute during COVID, as unemployment rates have dramatically understated the deterioration in the labor market, according to Federal Reserve Chairman Jerome Powell.

Using an alternative measure of unemployment offers a more comprehensive view of labor-market conditions by also including “discouraged workers” who have stopped searching for jobs and workers who are working part time but would like to have full-time jobs. By this measure, downturns are even more damaging to the labor market than what one would conclude from considering the conventional, and more widely reported, unemployment rate.

The Facts

The most widely reported unemployment rate is officially known as U3 unemployment and represents the number of people who are unemployed as a percentage of the labor force. For the purposes of U3, the unemployed are defined as those people who do not have a job, have been actively looking for work over the past four weeks and are currently available for work. People are considered employed if they did any paid work—this includes all part-time and temporary work as well as full-time employment. The labor force represents the sum of the unemployed and the employed (it excludes people living in institutions and active-duty military personnel).

The U3 unemployment rate is released on the first Friday (on April 2 this month) following the end of each month and is based on a survey of about 60,000 households rather than a full tally of the entire population. It is calculated by the Bureau of Labor Statistics using information from the Current Population Survey conducted by the Census Bureau.

Breaking news: U.S. gains 916,000 jobs in March, outrunning economists’ forecast and signaling a strengthening economy

The definitions of who is considered “employed” and “unemployed” for the purposes of U3 point to some shortcomings for using the U3 unemployment rate as an indicator of the overall strength of the labor market. If someone who is unemployed stops looking for a job (even if she would like to have one) then she is no longer counted as unemployed, nor is she counted as being in the labor force. This “discouraged worker” contributes to a decrease in the unemployment rate because when she drops out of the labor force and is no longer counted as an unemployed person there is a proportionally bigger decrease in the unemployed than in the labor force since so many more people are in the labor force than are unemployed.

For example, if there are 5 unemployed people in a labor force of 100, and one of the unemployed drops out of the labor force, the unemployment rate goes from 5% to 4.04% (4/99 = .0404). The U3 unemployment rate will also fail to reflect a situation where someone who was working full time, and would like to continue to do so, is forced by economic conditions to work part time. This situation would not lead to any change in the U3 unemployment rate even though that person is now underemployed.

An alternative measure, the U6 unemployment rate, sometimes referred to as the “underemployment rate,” offers a broader indicator of labor market underutilization. The U6 unemployment rate differs from the U3 unemployment rate in several ways. It adds to the U3 definition of the unemployed those who are working part time for economic reasons and workers “marginally attached to the labor force”—which is defined as those who are not working and have not looked for work in the past four weeks but have looked for work in the past 12 months. Broadening the measure to include these workers makes the U6 unemployment rate higher than the U3 unemployment rate.

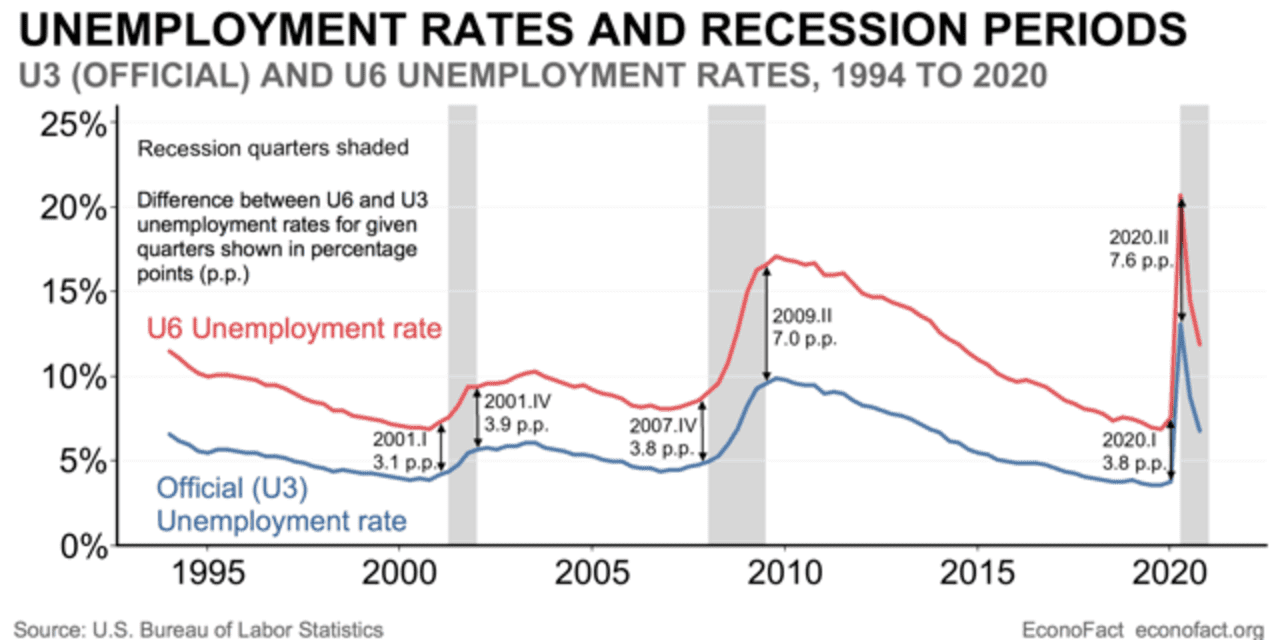

The average U6 unemployment rate is almost 80% higher than the official (U3) unemployment rate since 1994 (see chart). The Bureau of Labor Statistics began publishing the U6 unemployment rate in 1994. Its average value since that time is 10.4%. The average official unemployment rate over this period is 5.8%. In February 2021, the official unemployment rate was 6.2% and the U6 unemployment rate was 11.1%. With a civilian labor force of about 160 million people, this translates to 17.8 million underemployed, of which 9.9 million are counted as officially unemployed—so there are about 7.9 million people who are unemployed by the U6 definition but who are not counted as officially unemployed by the U3 definition.

The difference in the U6 and U3 unemployment rates is not constant but tends to move with the business cycle, increasing when the economy is in a recession. It had been thought that the gap between U6 and U3 was relatively stable, but this has not turned out to be the case in the more recent past.

For instance, before the Great Recession, a Bureau of Labor Statistics report stated: “While the alternative measures differ in magnitude from the official unemployment rate, they typically show very similar movements over the course of the business cycle.” However the difference between U3 and U6 has expanded during each of the three recessions that have taken place since 2000: the relatively mild recession that began in the second quarter of 2001, the Great Recession that began in the first quarter of 2008, and the current recession that began in the second quarter of 2020 (see chart, the gray shaded areas represent periods when the economy was in a recession as determined by the National Bureau of Economic Research). This gap reached 7.6 percentage points in the second quarter of 2020, its largest value since the introduction of the U6 unemployment rate. The figure also shows that the gap between the measures narrowed during periods when the economy was stronger.

Statistical analysis confirms the significant responsiveness of the difference between the U6 and U3 unemployment rates to business-cycle conditions. It is well known that the U3 unemployment rate increases when the economy is operating below its full potential. This relationship is known as Okun’s Law. We estimated a form of Okun’s Law for the U6 unemployment rate as well. We find that the U6 unemployment rate is even more responsive to the economy operating below potential than the U3 unemployment rate.

More specifically, we find that a one-percentage point worsening of business cycle conditions is typically associated with about a 0.62 percentage point increase in the difference between the U6 and U3 unemployment rates. But this estimate falls short of explaining what happened in the second quarter of 2020 by a full percentage point, demonstrating that this was a particularly fraught time in the labor market.

What This Means

The official (U3) unemployment rate is one of the most widely watched economic statistics, but it offers a more limited view of labor-market conditions than broader indicators like the U6 unemployment rate, which takes into account those forced to work part time for economic reasons and those who have stopped looking for work in the past month.

Our original research demonstrates that the difference between these two measures of unemployment widens in an economic downturn—which means that the degree to which the conventional U3 unemployment rate underestimates labor-market distress increases during a recession.

As Chairman Powell suggested in his remarks in February, this means that the official unemployment rate fails to account for the full range of labor-market weakness, especially during a recession, and even more so during the current downturn.

There are important implications of this—if the choice of whether to continue extraordinary support for people hurt by this recession is based on the official unemployment rate rather than a broader measure, like the U6 unemployment rate, then policy may fail to step up to match labor-market weakness marked by workers who have been forced to part-time employment or who have stopped actively looking for a job.

This commentary was originally published by Econofact—How Weak is the Labor Market?

Christopher F. Baum is a professor of economics and social work at Boston College, and is chair of the Economics Department. His expertise is in applied econometrics, public health and financial economics. Follow him @cfbaum.

Michael Klein is a professor of international economic affairs at the Fletcher School of Law and Diplomacy at Tufts University. His research interests include world capital markets, exchange rate management, and foreign direct investment. Follow him @MKlein

April 04, 2021 at 02:51AM

Christopher F. Baum, Michael W. Klein

http://www.marketwatch.com/news/story.asp?guid=%7B21005575-02D4-D4B5-4572-D35699D4D97C%7D&siteid=rss&rss=1

Labels: Top Stories

0 Comments:

Post a Comment

Subscribe to Post Comments [Atom]

<< Home