Yen Recovers as Markets Extend Corrective Pattern

Yen Recovers as Markets Extend Corrective Pattern

The forex markets are extending near term corrective moves today, with Yen turning slightly stronger, followed by Swiss Franc. Canadian Dollar and Sterling are the weaker ones, followed by Dollar. The Loonie will look into BoC policy decision for guidance. Meanwhile, broader markets will look at development in overall risk sentiments. European indexes are trading slightly lower but US futures point to high open.

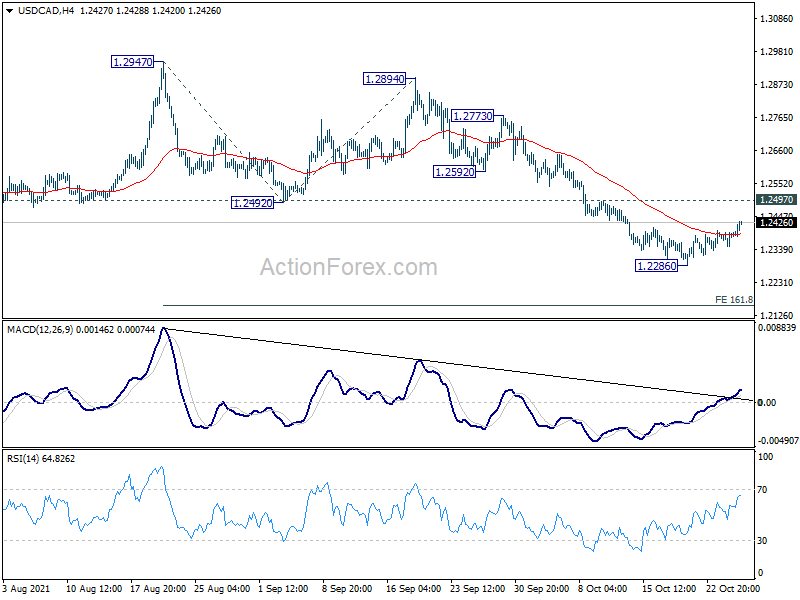

Technically, USD/CAD would be a focus in US session. While recovery from 1.2286 is extending, there is no change in the view that it’s just a corrective recovery. As long as 1.2497 resistance holds, larger fall from 1.2947 should still resume, sooner or later, through 1.2286 to 161.8% projection of 1.2947 to 1.2492 from 1.2894 at 1.2158 next. However, break of 1.2497 wall bring even stronger rebound. We’ll see which one it goes.

In Europe, at the time of writing, FTSE is down -0.14%. DAX is down -0.35%. CAC is down -0.25%. Germany 10-year yield is down -0.0573 at -0.173. Earlier in Asia, Nikkei dropped -0.03%. Hong Kong HSI dropped -1.57%. China Shanghai SSE dropped -0.98%. Singapore Strait Times rose 0.42%. Japan 10-year JGB yield dropped -0.006 to 0.098.

US durable goods orders dropped -0.4% mom in Sep, ex-transport orders rose 0.4% mom

US durable goods orders dropped -0.4% mom to USD 261.3B in September, better than expectation of -1.1% mom. Ex-transport orders rose 0.4% mom, matched expectations. Ex-defense orders dropped -2.0% mom. Transportation equipment dropped -2.3% to USD 77.7B.

Also released, goods trade deficit came in at USD -93.6B in September, smaller than expectation of USD -88.2B. Goods exports dropped USD -7B to USD 142.2B. Goods imports rose USD 1.1B to USD 238.4B. Wholesale inventories rose 1.1% mom to USD 739.5B. Retail inventories dropped -0.2% mom to USD 602.9B.

Germany downgrades 2021 growth forecast to 2.6%, upgrades 2022 to 4.1%

German government cut 2021 economic growth forecast sharply to just 2.6%, comparing to April’s expectation of 3.5%. Economy Minister Peter Altmaier said the downgrade was partly due to supply bottlenecks and rising energy prices, particularly for gas.

Nevertheless, for 2022, growth forecast was upgrade from 3.6% to 4.1%, as the supply bottlenecks ease. Growth is expected to normalize to 1.6% in 2023.

“The precondition is that we stabilize international supply chains, and, for example, make sure that more of the chips are produced that are built into almost every device, especially cars,” Altmaier said earlier in an interview with ARD television.

Germany Gfk consumer sentiment rose to 0.9, defying increasing inflation

Germany Gfk consumer sentiment for November rose to 0.9, up from 0.4, above expectation of -0.4. For October, economic expectations dropped from 48.5 to 46.6. Income expectations dropped sharply from 37.4 to 23.3. Propensity to buy rose from 13.4 to 19.4.

“This second increase to consumer sentiment in a row defies increasing inflation. German citizens are clearly expecting further price increases. That is why they consider to make purchases, in order to avoid even higher prices”, explains Rolf Bürkl, GfK consumer expert. “If the surge in prices continues, it would put a strain on consumer sentiment and a fundamental recovery would likely be further delayed.”

Also released, Eurozone M3 money supply rose 7.4% yoy in September, below expectation of 7.7% yoy. Swiss Credit Suisse economic expectations dropped from 25.7 to 15.6 in October.

Australia trimmed mean and weighted median CPI rose to highest in over 5 yrs

Australia CPI rose 0.8% qoq in Q3, matched expectations. Over the 12-month period, headline CPI slowed from 3.8% yoy to 3.0% yoy. Trimmed mean CPI jumped from 1.6% yoy to 2.1% yoy. Weighted median CPI rose from 1.6% yoy to 2.1% yoy too. Both trimmed mean and weighted mean CPI readings were highest in over five years, and the first annual movements above 2% since September 2015 quarter.

Head of Prices Statistics at the ABS, Michelle Marquardt said the most significant price rises in the September quarter were new dwellings (+3.3 per cent) and automotive fuel (+7.1 per cent).

New Zealand reports record imports and trade deficit in Sep

New Zealand goods exports rose 10% yoy or NZD 387B to NZD 4.4B in September. Goods imports rose 30% yoy or NZD 1.5B to NZD 6.6B. Trade deficit came in at NZD -2.2B, versus expectation of NZD -0.8B. The set of data marked the third successive month of record imports, resulting in a record trade deficit.

Exports to China rose 25%, to Australia dropped -8.4%, to US rose 23%, to EU rose -10%, and to Japan dropped -5.5%. Imports from China rose 48%, from EU rose 29%, from Australia rose 28%, from US dropped -2.1%, from Japan rose 41%.

“These three consecutive record months for imports are a reflection of both the higher prices New Zealanders are paying for consumer goods, and strong demand for capital goods such as machinery used in construction, and passenger vehicles,” international trade manager Alasdair Allen said.

New Zealand ANZ business confidence dropped to 13.4 in Oct

New Zealand ANZ Business Confidence was finalized at -13.4 in October, down from September’s -7.2. Own Activity Outlook rose from prior month’s 18.2 to 21.7. Export intentions rose from 7.4 to 8.6. Investment intentions rose from 9.2 to 13.8. Employment intentions dropped from 14.1 to 10.9. Cost expectations rose from 84.2 to 87.2. Pricing expectations rose from 58.1 to 65.5. Inflation expectations rose further from 3.02 to 3.45.

ANZ said: “Despite living week to week to some extent, firms appear to be getting on with it as best they can. There are clearly challenges, with costs extremely high and profits expected to fall, but more positively, activity expectations, investment intentions and employment intentions are holding up. The COVID situation remains unpredictable, however, and we’ll be watching closely for any evidence of that uncertainty derailing plans.”

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.79; (P) 114.05; (R1) 114.41; More…

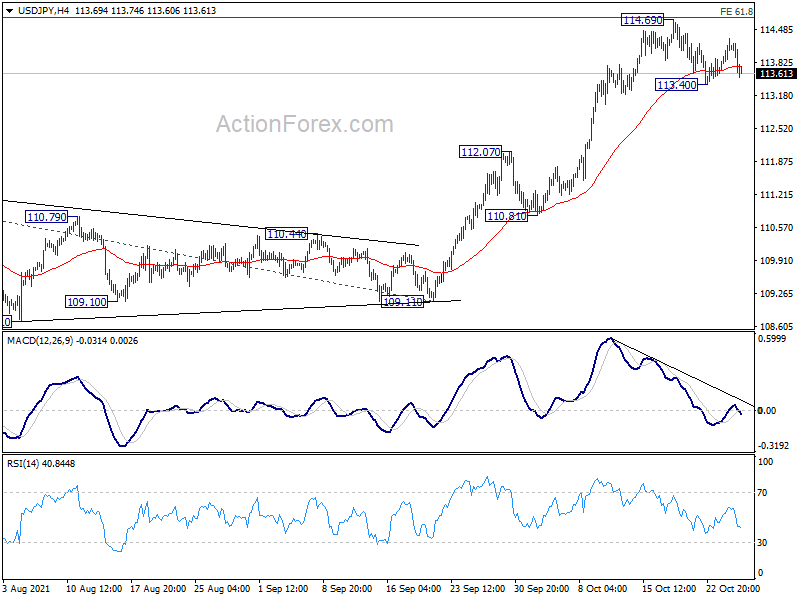

Intraday bias in USD/JPY remains neutral for the moment. Break of 113.40 minor support will bring deeper pull back. But downside should be contained above 112.07 resistance turned support to bring rebound. On the upside, firm break of 114.69 will resume the larger up trend to 100% projection of 102.58 to 111.65 from 109.11 at 118.18 next.

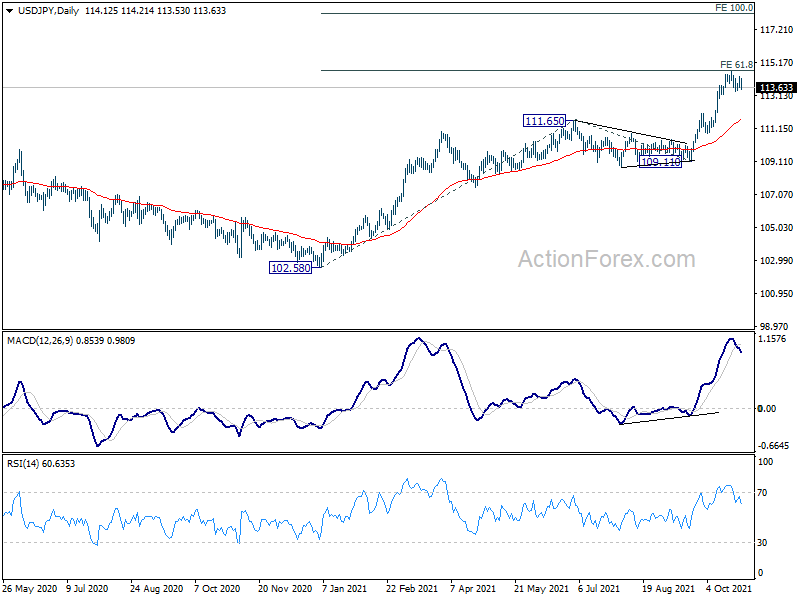

In the bigger picture, corrective decline from 118.65 (2016 high) should have completed at 101.18 already. Rise from the 102.58 is seen as the third leg of the up trend from 101.18. Next target is 114.54 resistance and then 118.65 high. This will now be the preferred case as long as 109.11 support hold, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Sep | -2171M | -762M | -2144M | -2139M |

| 23:01 | GBP | BRC Shop Price Index Y/Y Sep | -0.40% | -0.50% | ||

| 00:00 | NZD | ANZ Business Confidence Oct | -13.4 | -8.6 | ||

| 00:30 | AUD | CPI Q/Q Q3 | 0.80% | 0.80% | 0.80% | |

| 00:30 | AUD | CPI Y/Y Q3 | 3.00% | 3.80% | 3.80% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | 0.70% | 0.50% | 0.50% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | 2.10% | 1.60% | 1.60% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Nov | 0.9 | -0.4 | 0.3 | 0.4 |

| 08:00 | CHF | Credit Suisse Economic Expectations Oct | 15.6 | 25.7 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Sep | 7.40% | 7.70% | 7.90% | |

| 12:30 | USD | Durable Goods Orders Sep | -0.40% | -1.10% | 1.80% | |

| 12:30 | USD | Durable Goods Orders ex Transportation Sep | 0.40% | 0.40% | 0.30% | |

| 12:30 | USD | Goods Trade Balance (USD) Sep P | -96.3B | -88.2B | -87.6B | |

| 12:30 | USD | Wholesale Inventories Sep P | 1.10% | 1.00% | 1.20% | |

| 14:00 | CAD | BoC Interest Rate Decision | 0.25% | 0.25% | ||

| 14:30 | USD | Crude Oil Inventories | 2.0M | -0.4M | ||

| 15:00 | CAD | BoC Press Conference |

Featured Analysis

Load moreLearn Forex Trading

Forex Forecasts: Basic Forex Forecasting Techniques

Inside the Forex Market: Fake News, Currency Wars & Corruption

Make An Honest Self Appraisal

Range Trading Explained

Trading the Forex Market Using Bullish and Bearish Pennants

How to Become a Forward-Thinking Forex Trader

October 28, 2021 at 01:18AM

ActionForex.com

https://ift.tt/3nyiUih

0 Comments:

Post a Comment

Subscribe to Post Comments [Atom]

<< Home